Understanding insurance and laser-related claims

Lasers are powerful but carry risks like burns or pigment changes. Careful patient selection, patch testing, and correct settings help reduce complications—and insurance offers protection if things go wrong.

Whether you’re removing unwanted hair, treating pigmentation, or rejuvenating skin, complications can occur with laser treatments. From burns and pigmentation changes to dissatisfied clients and unexpected reactions, the margin for error in light-based treatments can be narrow. That’s why having the right insurance isn’t just a recommendation – it’s a professional responsibility. In this chapter, we explore the realities of laser-related claims, the common pitfalls clinics face, and how to protect your practice with appropriate, specialist cover from Hamilton Fraser.

Laser claims

From January 2020 to November 2024, Hamilton Fraser handled over 1,096 aesthetic malpractice claims. Of these:

245 were related to dermal fillers

210 were laser-related claims

91 involved botulinum toxin

As you can see, laser treatments rank second only to dermal fillers in frequency of claims, which may surprise you. While many aesthetic treatments carry risks, the nature of laser treatments means those problems can be serious and that’s why you need to have rigorous protocols and comprehensive insurance in place.

Most common laser-related claims:

Burns and blistering due to incorrect settings, lack of cooling, or treating recently tanned skin

Hypopigmentation or hyperpigmentation, especially in patients with Fitzpatrick skin types IV–VI

Scarring linked to poor patch testing, overlapping pulses, or equipment malfunction

Client dissatisfaction stemming from unrealistic expectations or inadequate consultation

Burns remain the most frequent cause of laser claims. Common risk factors include:

Failure to re-patch test after device servicing or treating a new body area

Clients not disclosing recent sun exposure or retinoid use

Inadequate documentation of consultation, settings, or post-treatment advice

Using inappropriate wavelengths or treating contraindicated skin types

“Most of the claims we see come from hair removal and tattoo removal, often because settings are too high, or patch testing hasn’t been updated when treating a new area.Patch testing is sometimes missed when clients service their laser, change the headpiece or when they are patch testing a new area of the body. For example, if the client has already had laser hair removal to the face but now wants their legs done. For this reason, I would stress the importance of servicing your lasers, maintaining them and patch testing again if there are any changes in equipment or the patient’s circumstances.” — Priya Chander, Hamilton Fraser Claims Handler

To reduce your risk:

Conduct detailed skin assessments (including Fitzpatrick typing)

Document every patch test, setting, and aftercare instruction

Update records when patients return for new areas

Make sure device settings are recalibrated after servicing or hardware changes

Make sure that manufacturer guidelines are always followed

The BMLA has a comprehensive document outlining treatment guidelines for the use of laser and intense pulsed light devices for hair reduction and treatment of superficial vascular and benign pigmented lesions.

Read our guide to the biggest insurance payouts and claims trends in 2024 for more. Our Founder and CEO Eddie Hooker also wrote an article for Aesthetic Medicine on the topic.

Listen to our ‘Let’s talk laser’ podcast with leading laser and skincare expert, Debbie Thomas for more on this

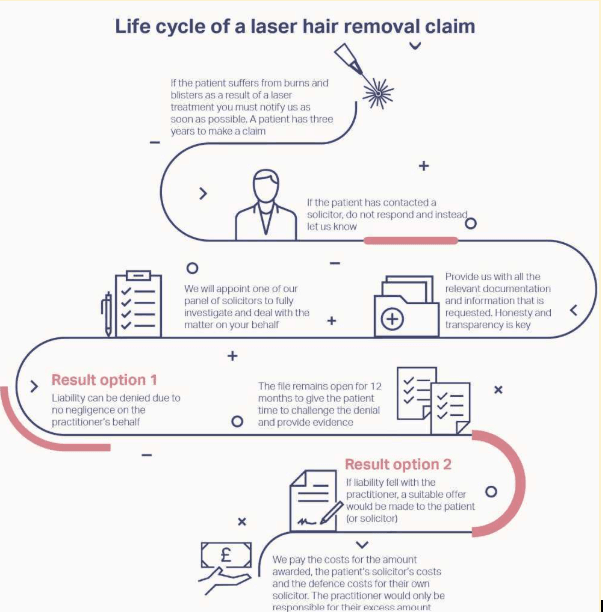

If a patient experiences an injury, even if they don’t immediately say they’ll make a claim, you must notify your insurer as soon as possible. Claims can be made up to three years after the treatment date, so early notification is essential.

In the event of a claim, Hamilton Fraser’s experienced claims team will collect all relevant information, including:

Treatment details (what, where, and when)

Practitioner notes and patient correspondence

Laser manual, protocol, and training certificates (for laser claims)

Any solicitor communications (if applicable)

You'll also be asked for a summary of events and whether you believe anything went wrong during treatment (e.g. incorrect settings). Being open and honest from the outset helps avoid delays and accurate liability assessment.

Once all documents are submitted, Hamilton Fraser will appoint a solicitor from its panel to investigate the claim. This may involve additional questions before the solicitor advises on whether liability should be admitted.

A few other important things to consider:

If you are VAT registered any VAT charged on a claim will need to be paid for by the business and subsequently reclaimed through your VAT returns.

If you are self-employed and work for a clinic, you are required to hold your own indemnity insurance. In the event of a claim arising from a procedure you performed, liability would typically be redirected to the self-employed practitioner. However, it can potentially be brought against both the practitioner and the business/clinic.

Remember, mistakes happen – that’s what your insurance is for. We're here to support you throughout the process.

Read more about the life-cycle of a laser hair removal claim here.

Not all insurance policies are created equal. Aesthetic practitioners should prioritise quality, scope of cover, and access to claims support – not just price.

Key things to look for:

FCA-regulated broker – makes sure you're working with a licensed, regulated insurer

Treatment-specific cover – confirm your policy lists laser and/or IPL

Device-specific cover – aligned with your exact system (e.g. Soprano Ice, Harmony, SmartXide)

Practitioner-specific – only trained professionals should be listed on the policy

Support access – policies should include legal guidance and claims management

“Insurance is only as good as its response when you need it.” – Eddie Hooker, Founder and CEO, Hamilton Fraser

Hamilton Fraser covers a wide range of laser and light-based treatments with tailored policies depending on the type of laser treatments you are offering.

Our Essential+ coverage includes non-invasive laser and LLLT devices, while the Laser category supports all machines excluding laser lipolysis.

Start protecting your laser and IPL treatments today – get an instant quote with Hamilton Fraser and make sure you're covered. For more advice, call 0800 63 43 881 or request a call back, and a member of our team will contact you to discuss your requirements.

Listen to our ‘Let’s talk laser’ podcast for an insightful discussion on this

Minimising risks like burns and pigmentation changes

Managing patient expectations and communication

Staying compliant with insurance, protocols, and device guidelines